Author Archive

by Wayne A. Thorp, CFA The last two installments of Spreadsheet Corner provided templates on how to calculate bond prices, returns and price sensitivity

16 Март, 2015 No Comment Read More

Bonds Duration interest coupons bond value

Bonds Duration interest coupons bond value

Advertisement Expert: Doug Ingram — 4/7/2000 Question How would you describe the duration and the convexity of a T-bond? In what way(s) are these

16 Март, 2015 No Comment Read More

BondEdge fixed income portfolio and credit risk analytics

BondEdge fixed income portfolio and credit risk analytics

The following article is reprinted from the Quarter 3, 2004 issue of On the Edge. the Interactive Data Fixed Income Analytics quarterly newsletter. Effective

16 Март, 2015 No Comment Read More

Bonds Duration Bond Duration Duration Bond

Bonds Duration Bond Duration Duration Bond

Bonds Duration What is Duration , how is it used,and whats its significance in finance ? We Answered: In any analysis of fixed income

16 Март, 2015 No Comment Read More

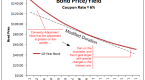

Contents Pricing a bond Bond prices are influenced by the credit quality of the issuer as well as marketplace changes in required yield. There

16 Март, 2015 No Comment Read More

BondEdge fixed income portfolio and credit risk analytics_1

BondEdge fixed income portfolio and credit risk analytics_1

The following article is reprinted from the Quarter 3, 2007 issue of On the Edge. the Interactive Data Fixed Income Analytics quarterly newsletter. Back-to-Basics:

16 Март, 2015 No Comment Read More

What does a bond duration measure? Duration is the weighted average term to maturity of a bonds cash flows and therefore, is a valuable

16 Март, 2015 No Comment Read More

Bond Duration Calculation Bond Duration Calculation Example

Bond Duration Calculation Bond Duration Calculation Example

Bond Duration Calculation Jo Said: In financial terms, how do you define and calculate Duration ? We Answered: Duration: change of 100 basis points.

16 Март, 2015 No Comment Read More

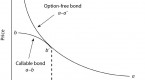

Bond Duration and Convexity Simplified – Part 2 of 2 Finance Train

Bond Duration and Convexity Simplified – Part 2 of 2 Finance Train

As we learnt in part 1. the duration, as measured by the slope of the curve, changes as yields change. The slope of the

16 Март, 2015 No Comment Read More

Bond Convexity What it is and How it Works

Bond Convexity What it is and How it Works

Bond convexity is a measure of how the duration of a bond changes when interest rates change. The concept of duration and convexity are

16 Март, 2015 No Comment Read More

Follow Us

Connect with Us

![]()

![]()

![]()

Sidebar Post

- Most Popular

- Recent Comments

Featured Posts

Popular Posts

- #1 Country For Tech StartUps U S A - by ip on 3-16-15

- Food technology startup YuMist raises Rs from VC firm Orios Venture Partners Economic - by ip on 3-16-15

- Mass exodus Tech startups may shift overseas as young ventures face regulatory hurdles in India - by ip on 3-16-15

- Number One Country For Tech StartUps U S A - by ip on 3-16-15

-

Bollinger Bands Strategy With 20 Period ...

-

Pay Off Your Mortgage Prior To Retiremen...

-

You Say You Want A Dissolution An Overvi...

-

Pay Down the Mortgage Before Retirement ...

-

Volume indicator

-

Uncover Value Opportunities Using the Pr...

-

The Strategic Sourceror Top Tips for Rec...

-

How to pay off debt

-

Recessionproofing retirement

-

Frontier Markets The New Emerging Emergi...